Key points

– The upcoming Budget is an ideal opportunity to reframe government policy to put the economy onto a stronger path. The latest global crisis adds to the case for this.

– The five key things the Budget needs to do are: limit any “cost-of-living” relief; cut government spending over four years; undertake serious tax reform and not just tax hikes; big productivity reforms like less red tape & more incentives to invest; and reform the Charter of Budget Honesty.

Introduction

As an economist working for an investment manager, Australian Federal Budgets can be tedious. They generate lots of fanfare along with a flurry of activity but invariably come and go with little impact on investment markets – all to be forgotten a few weeks later. But as the major Government policy event each year, they always have the potential to be something great. And that certainly applies to the coming 12th May Budget. First, the Treasurer has recognised that productivity needs to be boosted and that inflation is too high and so he committed to three reform packages in the Budget – around budget savings, productivity and tax reform. And this Budget is the first after the Government’s big election win last year that gave it a huge boost in political capital with the next election two years away. So, if the current Government is to focus on much needed reform now is the time to do it. But the oil supply shock flowing from the Iran War threatens to derail this and push the Government down a populist path of short term “cost-of-living” measures at the expense of reform. Hopefully not and the Treasurer has assured us that ambitious reform remains on the agenda! In fact, the latest global crisis highlights the need for a reform agenda to make the economy stronger. This note outlines the five key things the Budget needs to do.

#1 Limit any “cost-of-living” stimulus

Some sort of cost-of-living relief to deal with the impact of the War looks likely and direct transfers to households (like the Low and Middle Income Tax Offset) and key impacted businesses are preferrable to an extension to fuel tax cuts as the latter just blunt the price signal to cut back on fuel use. But the lesson from the GFC and pandemic is that any fiscal easing be timely such that it impacts when needed, targeted to those who really need it, temporary such that it cuts out as soon as the threat is passed and calibrated to the size of the threat. The pandemic stimulus was timely (but not well targeted) and was arguably more than needed, which contributed to the inflation problem we had when the economy reopened.

The problem now in designing any stimulus is twofold. First, while some stagflationary impact from the War looks baked in, whether it’s mild and short-lived (say 5% inflation and 1.5% growth) or more severe (say 8% inflation and recession) depends on how long the Strait of Hormuz remains blocked. In the last two weeks, it’s been declared open then shut twice. Our base case is that we are on the off ramp to peace – as Trump is under immense political pressure to end the War given the midterms and Iran likewise as the blockade of its oil revenue will intensify internal political discontent – and that the Strait will soon reopen. In this case any further stimulus should be minor (say no more than $5bn or 0.2% of GDP). But of course, the risk is very high that there won’t be a quick resolution, leaving us on the slippery slope to even higher oil prices (roughly $US150/barrel would be needed to reduce global oil usage by the 10-15% hit to oil supply) and fuel restrictions in Australia. This may then necessitate more stimulus.

The second problem is that the appropriate policy response is complicated by a supply shock which will add to inflation and fiscal stimulus could only make inflation worse. This will be at a time when the RBA will likely give priority to getting inflation down having learnt the lessons from the 1970s.

The bottom line is that any cost-of-living relief/economic stimulus should be modest & very well targeted to those who really need it (like low income earners and businesses with high energy cost exposure that could fold).

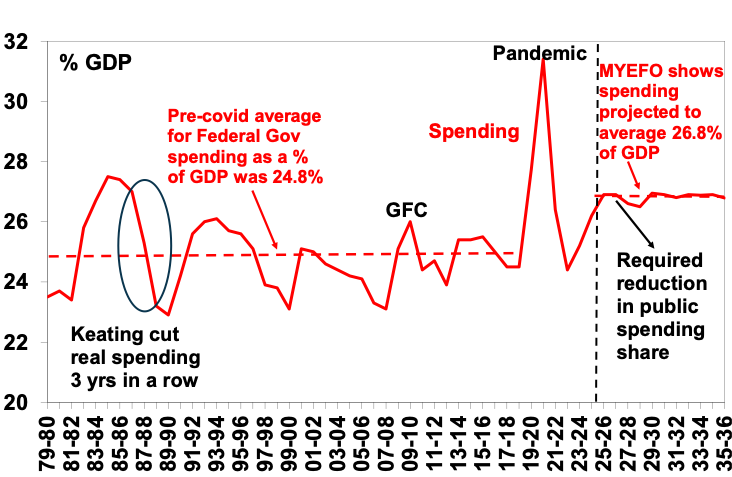

#2 Cut government spending by around $100bn

Beyond any near-term temporary stimulus, public spending needs to be cut as a share of GDP back to longer term norms. The pandemic and its aftermath have seen public spending (Federal, state and local) surge from a 40-year average of around 22.5% of GDP to 28%. This surge in public spending has left little room for a pickup in private spending – consumer, home building and business investment – such that when it occurred last year the economy quickly ran up against capacity constraints and hence a rebound in inflation. Federal spending has been part of this surge. The next chart shows Federal spending (which includes transfers to the states) as a share of GDP. Public spending as a share of GDP has risen from 24.3% in 2022-23 to a forecast 26.9% this financial year as a result of three years of nominal growth of 7-8%pa and it’s projected to settle at this higher share of the economy than pre-covid which will see capacity pressures sustained.

Federal Government spending

Source: Federal Treasury December MYEFO (page 57 and pages 316-317), AMP

Source: Federal Treasury December MYEFO (page 57 and pages 316-317), AMP

So, the key for the Budget is to cut spending over the next few years as a share of GDP to free up capacity in the economy and hence help ease inflation. Our assessment is that it needs to be brought back to around 25% of GDP which is in line with the longer-term norm. If this were to occur over the four years to 2029-30 it would entail cutting roughly $102bn out of Federal spending over four years and constraining spending growth to 3%pa. This would require cuts to the NDIS (with the Government looking like it might move in this direction), more aggressive cuts to the public service and more means testing of welfare.

This would also require the Government to “save” most of any new revenue windfall flowing from higher energy prices due to the War) and higher than expected iron ore and gold prices (which has been put at between $30-$60bn over the forward estimates) as it did in its first Budget in October 2022 when 81% of it was saved. It would also need to be more than just trickery using higher nominal GDP (flowing from higher inflation to temporarily lower the Government spending to GDP ratio).

#3 Serious tax reform and not just tax hikes

Media reports suggest the Government is considering various tax changes for the budget – reducing the capital gains tax discount, limiting the number of properties an investor can negatively gear, introducing a minimum tax on trusts, an export levy on gas producers and moving to a road user charge to include EVs. Each of these have merit: the capital gains tax discount is too generous; some make excessive use of negative gearing; trusts allow an unfair tax advantage; gas projects arguably receive an unfair advantage relative to petroleum projects (although the existing Petroleum Resources Rent Tax should be reformed to make it fairer rather than a new tax imposed); and EVs have an unfair advantage as they don’t pay fuel excise. But if this is all the Budget has on tax, it will be a tax hike and not real tax reform. Real tax reform should address four key issues.

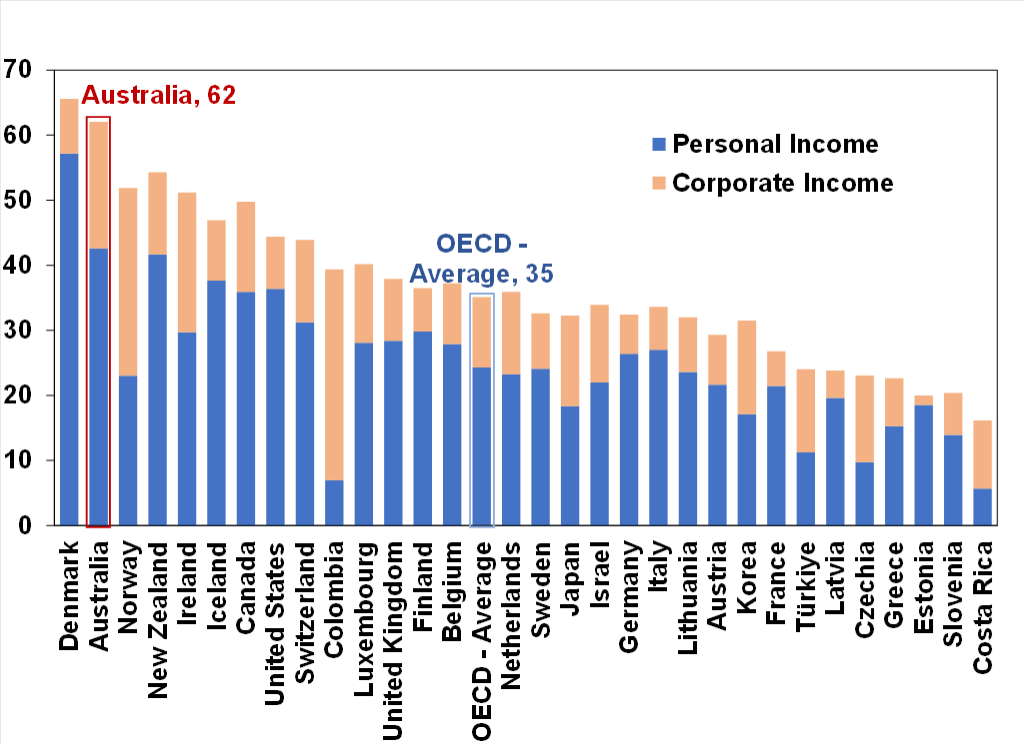

First, the Australian tax system is excessively reliant on income tax. Income tax is 62% of tax collections versus the OECD average of 35%.

Income tax as % of total tax revenues

Source: OECD, AMP

Source: OECD, AMP

Income tax is highly distortionary – as it impacts decisions to work and invest – whereas a GST levied at the same rate on all items is far less distortionary. So, a GST is a far more “efficient” tax than income tax and a greater reliance on it versus income tax will boost productivity. The high reliance on income tax also creates equity issues as the aging population will see an increasing burden placed on younger workers to foot rising health and aged care bills whereas self-funded retirees are taxed lightly.

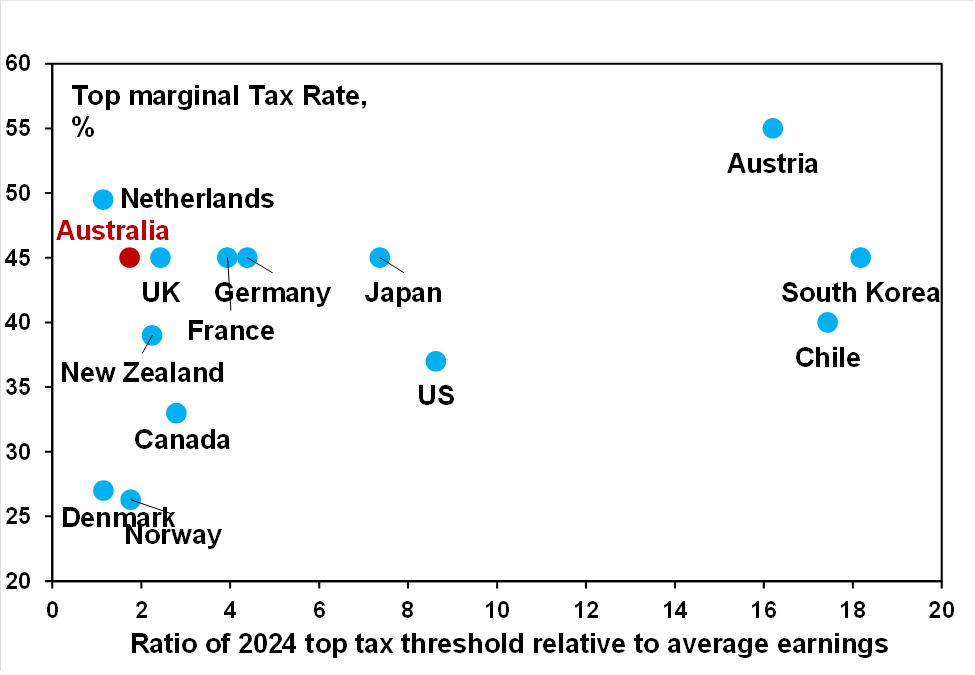

Third, the Australian tax system is highly progressive. The current top marginal tax rate at 47% is above the median of comparable countries and kicks in at a relatively low multiple of average weekly earnings. This is reflected in the top 5% of taxpayers paying around 37% of personal income tax collections and the top 10% paying nearly 50% of income tax. This likely discourages work effort and hence productivity. So, while the tax system is complicated with various concessions – that can be too generous or lead to inequities – curtailing access to them (as is being considered in relation to capital gains, negative gearing and trusts) will only add to the burden on a relatively small group and act as a disincentive for work effort when we should be doing the opposite.

Global individual tax rates comparison

Source: OECD, AMP

Source: OECD, AMP

Thirdly, due to bracket creep, just keeping up with inflation can see a worker pushed into a tax bracket that was never intended for them and is currently being relied on by the Government to balance the budget over the next decade. The ideal solution is to index the tax brackets by 2.5% (the inflation target) each year. This will keep the Government accountable by forcing them to pass higher tax rates through Parliament if they want more tax revenue.

Finally, the tax system has numerous anachronisms, eg: the GST applies to a diminishing share of spending; states’ stamp duties distort property decisions and worsen affordability; payroll taxes discourage employment; and car tariffs are levied when there is no car industry to protect.

Just fiddling with a few tax concessions in the budget will amount to nothing more than a tax hike, will likely make the tax system even more progressive working against incentive and do little to relieve housing affordability (which is due to the housing undersupply) or intergenerational equity beyond appearances. What is needed is simple: much lower personal tax rates with higher thresholds; a lower corporate tax rate; a higher and more comprehensive GST; compensation of low-income earners and welfare recipients for increasing the GST; the indexation of tax brackets to inflation; and the removal of stamp duty and its replacement with land tax. The shift in reliance from income tax to GST is the best way to improve intergenerational equity. This would take political courage, but is the direction we should be moving in.

#4 Significant productivity reforms

Productivity growth (or growth in output per hour worked) is the key to growth in living standards over time but unfortunately it has stalled over the last decade. Reinvigorating it is critical to boosting living standards but also to expanding the capacity of the economy to accommodate growth without adding to inflation. Limiting public spending (to make room for more productive private spending) and fundamental tax reform are critical but it requires a whole bunch of other things (here is a short list). In particular, it’s critical that the Budget have a focus on product and labour market deregulation to remove red tape, boost flexibility and make it easier to get things done and to provide more incentives for companies to invest.

#5 Reform the Charter of Budget Honesty

This is necessary to refocus attention on the headline budget deficit given the widening use of “off budget” spending on the grounds that it’s an “investment” but which still adds to public debt. It should also be a requirement that such “investments” – often undertaken on the grounds of “making more things here” or boosting “supply chain resilience” – are assessed on a cost-benefit basis by an independent authority like the Productivity Commission.

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Important note: While every care has been taken in the preparation of this document, neither National Mutual Funds Management Ltd (ABN 32 006 787 720, AFSL 234652) (NMFM), AMP Limited ABN 49 079 354 519 nor any other member of the AMP Group (AMP) makes any representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided. This document is not intended for distribution or use in any jurisdiction where it would be contrary to applicable laws, regulations or directives and does not constitute a recommendation, offer, solicitation or invitation to invest.